Understanding the investment life cycle is crucial for anyone looking to maximize their returns. As an investor, it’s important to know the different stages of the investment life cycle and the strategies that can be employed to maximize returns at each stage. In this article, we will explore the investment life cycle and provide personalized advice on how to maximize returns based on your financial goals, risk tolerance, and investment portfolio.

In this roleplay scenario, you will be meeting with a financial advisor for a one-on-one consultation. The advisor will discuss the different stages of the investment life cycle and provide personalized advice on how to maximize returns at each stage. We will cover topics such as asset allocation, diversification, risk management, and tax planning, and provide case studies and real-life examples to illustrate the concepts and strategies discussed. So, let’s dive in and learn how to maximize your returns through the investment life cycle.

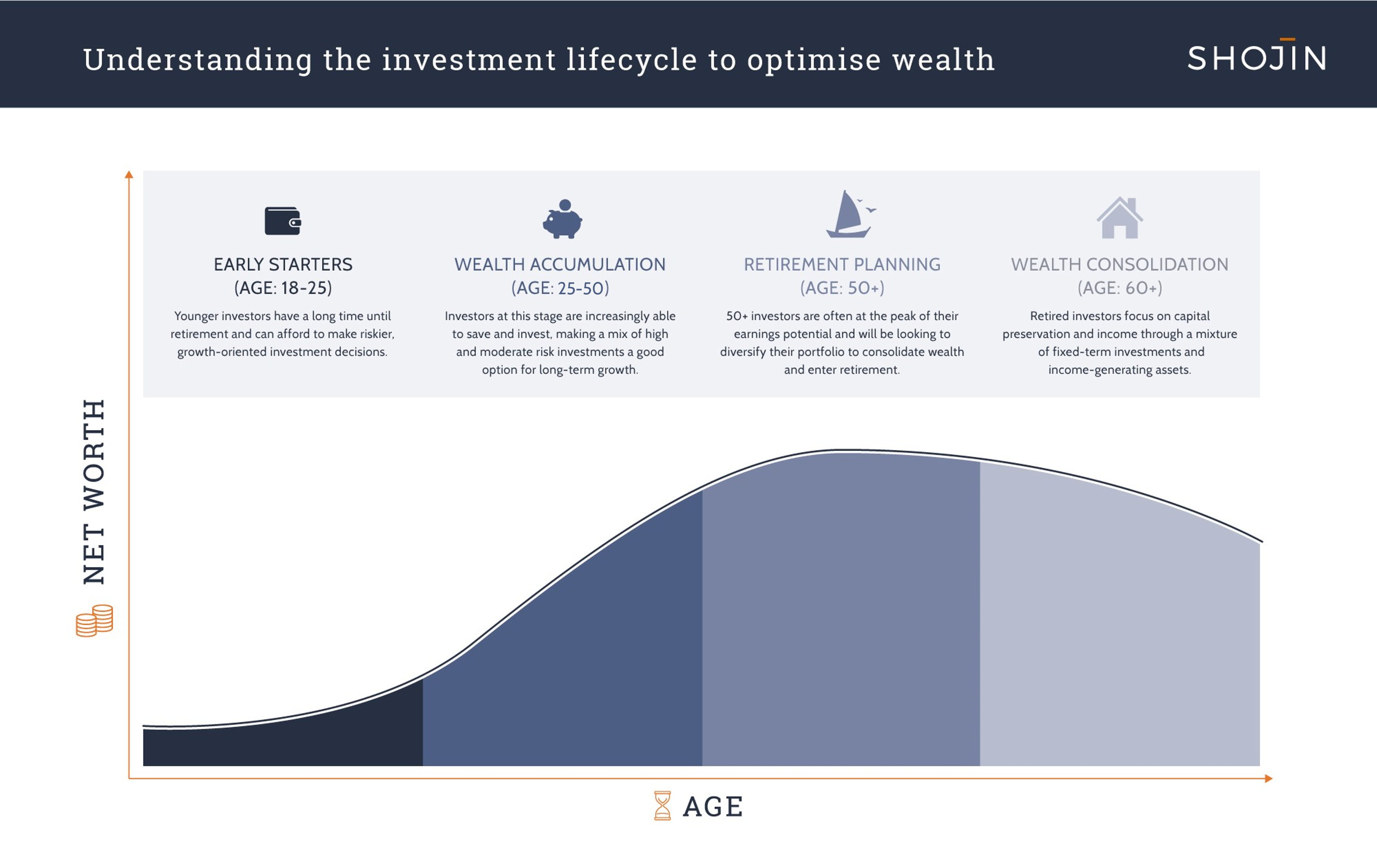

What is the Investment Life Cycle?

The investment life cycle refers to the different stages an investor goes through in their financial journey. These stages include the accumulation phase, consolidation phase, and retirement phase. During the accumulation phase, investors focus on building their investment portfolio and maximizing returns through strategies such as dollar-cost averaging and investing in growth-oriented assets. The consolidation phase is characterized by a shift towards more conservative investments and a focus on preserving wealth. Finally, during the retirement phase, investors prioritize generating income from their investments to support their lifestyle. Understanding the investment life cycle is crucial for investors to make informed decisions and maximize returns at each stage.

Stage 1: Accumulation Phase

During the accumulation phase, investors are typically in the early stages of their careers and have a longer investment horizon. This stage is characterized by a focus on growth and accumulation of assets. Strategies for maximizing returns during this phase include investing in growth-oriented assets such as stocks and mutual funds, taking advantage of tax-deferred retirement accounts, and regularly contributing to investment accounts. Case studies and real-life examples can illustrate the benefits of starting early and consistently contributing to investment accounts, as well as the potential risks of not taking advantage of tax-deferred retirement accounts.

Stage 2: Consolidation Phase

The consolidation phase is characterized by a shift from growth to preservation of assets. Investors in this phase are typically in their mid-career and have accumulated a significant amount of assets. Strategies for maximizing returns during this phase include diversifying the investment portfolio, rebalancing the portfolio regularly, and considering alternative investments such as real estate or private equity. Case studies and real-life examples can illustrate the benefits of diversification and the potential risks of not rebalancing the portfolio regularly.

Stage 3: Retirement Phase

During the retirement phase, investors shift their focus from accumulation and growth to income generation and preservation of capital. Strategies for maximizing returns during this phase include investing in income-generating assets such as bonds and dividend-paying stocks, considering annuities or other guaranteed income products, and managing tax liabilities. Case studies and real-life examples can illustrate the benefits of a well-diversified income portfolio and the potential risks of not managing tax liabilities effectively.

Overall, personalized advice from a financial advisor can help investors navigate each stage of the investment life cycle and maximize returns based on their individual financial goals, risk tolerance, and investment portfolio.

As a financial advisor, I believe that understanding the investment life cycle is crucial for maximizing returns. In the consolidation phase, investors typically have a larger portfolio and may be more risk-averse. Therefore, it’s important to focus on diversification and risk management strategies to protect their assets while still generating returns.

One strategy I often recommend during the consolidation phase is to invest in a mix of stocks and bonds. This can help balance risk and return, as stocks tend to have higher returns but also higher risk, while bonds have lower returns but are less risky. Additionally, I may suggest investing in alternative assets such as real estate or commodities to further diversify the portfolio.

Another important factor to consider during the consolidation phase is tax planning. Investors may have accumulated significant gains in their portfolio, and it’s important to minimize the tax impact of those gains. This can be achieved through strategies such as tax-loss harvesting or investing in tax-advantaged accounts like IRAs or 401(k)s.

Overall, personalized advice is key during the consolidation phase to ensure that investors are maximizing returns while also managing risk and minimizing taxes. As a financial advisor, I work closely with my clients to understand their financial goals, risk tolerance, and investment portfolio to provide tailored advice that meets their unique needs.

As a financial advisor, I believe that understanding the investment life cycle is crucial for maximizing returns. In the retirement phase, investors need to focus on generating income and preserving capital. This means that they should shift their portfolio towards more conservative investments, such as bonds and dividend-paying stocks.

During the consolidation phase, investors should focus on preserving their wealth and minimizing risk. This means that they should diversify their portfolio across different asset classes and sectors, and consider using strategies such as dollar-cost averaging and rebalancing.

In the accumulation phase, investors have a longer time horizon and can afford to take more risk. This means that they should focus on growth-oriented investments, such as stocks and mutual funds. They should also consider using tax-advantaged accounts, such as IRAs and 401(k)s, to maximize their returns.

When providing personalized advice, I take into account each investor’s financial goals, risk tolerance, and investment portfolio. I use a variety of tools and strategies to help them achieve their objectives, such as asset allocation models, risk assessment questionnaires, and tax planning software. I also provide ongoing support and guidance to help them stay on track and adjust their portfolio as needed.

Overall, I believe that working with a financial advisor can help investors navigate the different stages of the investment life cycle and maximize their returns. By providing personalized advice and guidance, we can help them achieve their financial goals and secure their financial future.

understanding the investment life cycle is crucial for maximizing your returns. By recognizing the different stages of the cycle, investors can make informed decisions about when to buy, hold, or sell their investments. It is important to remember that each stage of the cycle presents unique opportunities and challenges, and investors must be prepared to adapt their strategies accordingly. Additionally, diversification and risk management are key components of a successful investment plan, as they can help mitigate potential losses and maximize long-term gains.

To summarize, the main conclusions of this article are:

1. Understanding the investment life cycle is essential for maximizing returns.

2. Each stage of the cycle presents unique opportunities and challenges.

3. Diversification and risk management are crucial components of a successful investment plan.